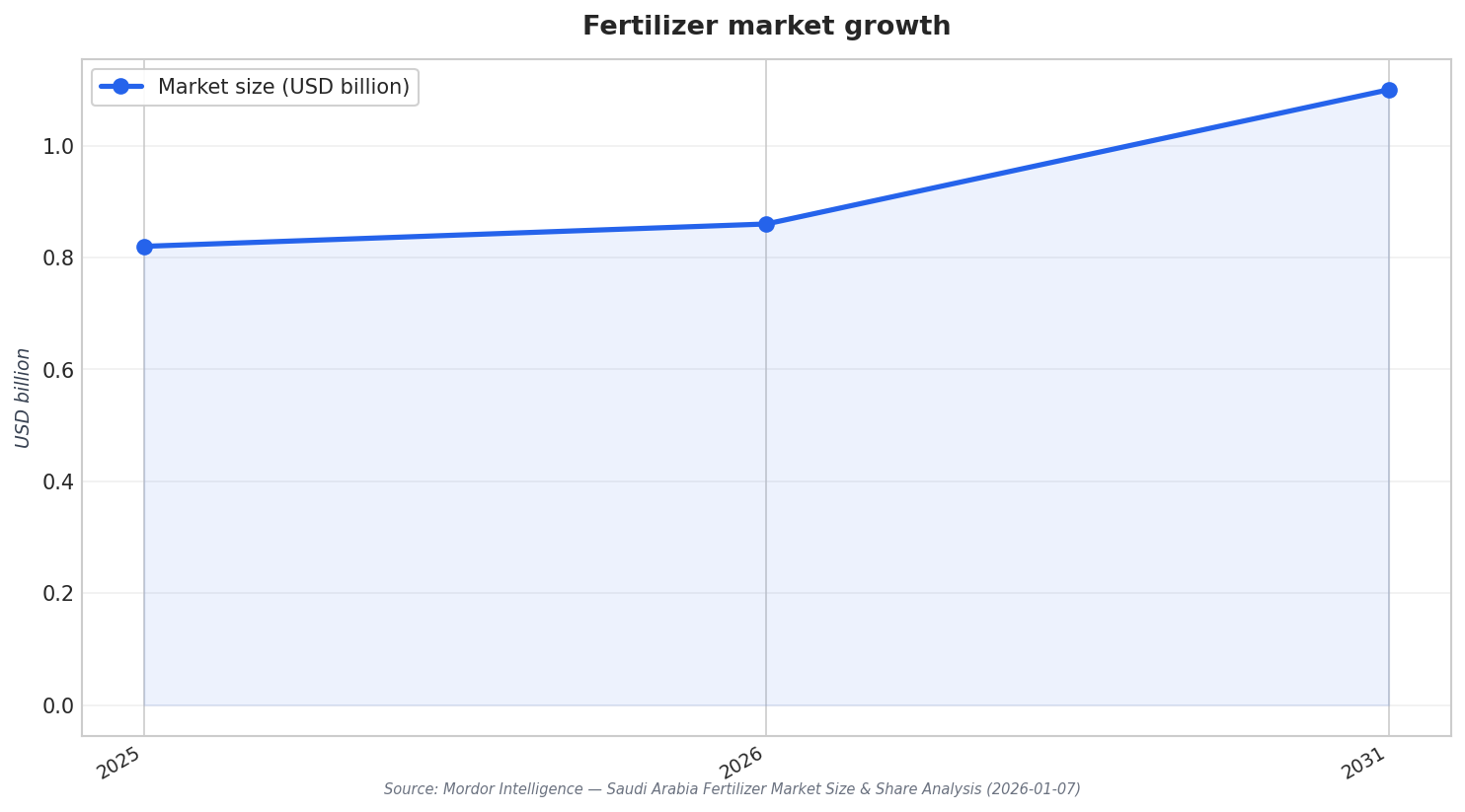

Saudi Arabia’s fertilizer market is on a measurable upward track, and that trajectory shapes the conversation around potash potential. Mordor Intelligence estimates the Saudi Arabia fertilizer market at USD 0.86 billion in 2026, up from USD 0.82 billion in 2025, with a projection of USD 1.1 billion by 2031 at a 5.03% CAGR over 2026–2031. The same report highlights that straight fertilizers held 70.35% share in 2025, while complex fertilizers are forecast to expand at a 6.53% CAGR through 2031. Those figures do not prove new domestic potash supply, but they do show a growing, segmenting market where potassium-based products could be pulled along by broader fertilizer demand growth.

Policy and investment signals matter because potash is primarily a fertilizer input, and Saudi demand growth is closely tied to food security. GMI Research states that around 80% of the country’s food requirements are met through imports, and it describes a two-pronged approach focused on improving local production while strengthening supply chains. In 2023, the Agricultural Development Fund announced SAR 1.5 billion in funding to support farmers to grow vegetables and related crops. In parallel, the same source reports Saudi Arabia captured more than 45% of production share in the GCC fertilizer market, and it cites 36.7 million tons of fertilizers produced in GCC countries. These points frame why local and regional fertilizer strategies can increase interest in potassium nutrients.

What Potash Demand Could Ride On Inside the Kingdom

Within Saudi Arabia, demand growth drivers lean heavily toward improved agronomy and efficiency, which may favor more balanced nutrition programs that include potash. Mordor Intelligence links market development to increased adoption of precision irrigation and notes research support for desert-soil bio-enhanced fertilizers. In terms of format, granular products had a 61.90% share in 2025, while liquid formulations are projected to lead growth at a 7.12% CAGR between 2026 and 2031. Crop-wise, grains and cereals held 37.45% of the 2025 market, and fruits and vegetables are advancing at a 6.62% CAGR to 2031. Separately, a market journal write-up attributes rising interest in phosphatic and potash fertilizers to precision agriculture and the need for balanced crop nutrition, while noting nitrogen fertilizers dominate due to natural gas feedstock advantages.

Any discussion of potash opportunity also needs global context, because pricing, product types, and supply concentration are shaped by international dynamics. Precedence Research sizes the global potash fertilizers market at USD 23.11 billion in 2025, rising to USD 24 billion in 2026 and projected to reach approximately USD 33.59 billion by 2035, expanding at a 3.81% CAGR from 2026 to 2035. The same source states that over 90% of potash produced globally is used as fertilizer for food crops and estimates approximately 64.6 million tons of potash were produced globally in 2022. It also notes potassium chloride dominated by type in 2025, while potassium sulfate is expected to grow at a significant rate. For potash exploration in Saudi Arabia, those global benchmarks clarify why potassium products can attract attention when local agriculture and fertilizer consumption are being actively promoted.

Saudi Arabia’s near-term fertilizer narrative is not only about nutrients; it is also about sustainability-linked exports and industrial capability, which can indirectly support broader fertilizer value chains. Mordor Intelligence reports that Saudi Aramco completed the world’s first certified bulk shipment of low-carbon ammonia to Japan in 2024, exporting 40 metric tons, and it adds that the Kingdom aims to produce 11 million metric tons of blue ammonia by 2030. The report also states producers can obtain 15–20% price premiums compared to conventional ammonia while meeting carbon emission standards of importing countries. While ammonia is not potash, these figures show the scale of Saudi ambition in fertilizers and inputs, and they set a backdrop in which potash exploration Saudi Arabia may be evaluated as part of a larger push for food security, local production focus, and investable industrial projects.

How big is Saudi Arabia’s fertilizer market, according to the cited estimates?

What does the sources say about fertilizer types and forms in Saudi Arabia?

What food security signals could influence potash demand in Saudi Arabia?

What global figures help frame the potash opportunity discussed in the article?

What does the article conclude about potash exploration in Saudi Arabia?