Saudi Arabian Mining Company (Maaden) completed a dollar-denominated international sukuk offering valued at $1 billion, described as an important step to enhance financial flexibility while the company expands its mining asset portfolio inside and outside the Kingdom. The issuance forms part of an international sukuk program aimed at attracting qualified investors from within Saudi Arabia and abroad. Maaden set the sukuk yield at 5.250% per annum with a maturity of 10 years, positioning it as long-term financing in international markets. The deal also illustrates how mining economics can be paired with Sharia-compliant structures that target both religiously aligned and secular institutions seeking asset-backed exposure.

The structure and distribution choices were built for cross-border participation. The sukuk was listed on the London Stock Exchange International Securities Market, and the sale process was conducted under Regulation S and Rule 144A of the US Securities Act of 1933, as amended, which the company said are standards that help reach a broad base of global investment institutions. Maaden issued 5,000 sukuk, each with a nominal value of $200,000. The offering documents also set out pre-defined cases in which redemption may occur, under the terms and conditions of the issuance. Together, these features show how a mining issuer can package long-duration funding in a format global institutions are set up to buy.

Why This Mining Sukuk Matters for Islamic Finance’s Global Reach

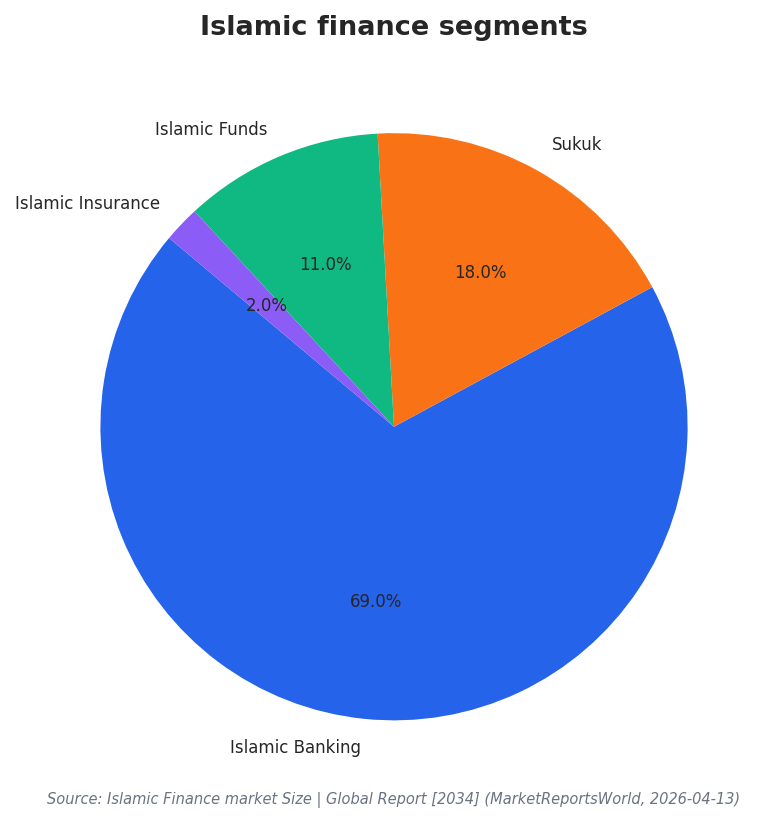

Maaden’s transaction lands in a market where sukuk is increasingly described as mainstream. The LSEG Islamic Investment Review 2025 cited a sukuk value of $1 trillion and reported $292 billion of sukuk issuance in 2025. The same review also referenced $40 trillion in Shariah-compliant market capitalization and $223 billion in Islamic funds value, framing a broader ecosystem that can support scaled funding channels. In parallel, a separate perspective on market composition said Islamic banking leads at 69%, with sukuk at 18%, Islamic funds at 11%, and Islamic insurance at 2%. For global mining investors, these figures signal depth across asset classes and a debt-capital tool that has moved beyond niche issuance.

Investor relevance also comes from how sukuk returns are framed. A sukuk structure is commonly described as representing partial ownership of an underlying asset, with investors earning a share of profits from that asset, rather than receiving fixed interest payments as in conventional bonds. This difference is tied to the prohibition of riba, or interest, and it is one reason sukuk can broaden participation for institutions and individuals seeking Sharia-compliant exposure. In Uganda, for example, a capital-markets official said roughly 13% of the population adheres to Islamic principles, noting that conventional capital markets can exclude this segment and that instruments like sukuk can broaden inclusion. That inclusion logic can translate into wider investor pools when issuances are offered internationally.

For the Maaden sukuk Islamic finance case study, the takeaway is not only the coupon and tenor, but also how the transaction was positioned for global mining capital. One analysis described Maaden’s $1 billion sukuk, with a 5.25% coupon and 10-year maturity, as a compelling example of how mining companies can access international capital markets through Islamic finance channels. It also highlighted that the combined use of a London listing plus Regulation S and Rule 144A enables broad institutional participation across global markets. As more major investment banks maintain dedicated Islamic finance capabilities and more institutions seek stable, asset-backed returns, this type of structure can help connect global investors to mining-sector exposure through compliant formats.

What were the main terms of Maaden’s international sukuk?

How did Maaden make the sukuk accessible to global institutions?

How does sukuk differ from conventional bonds in how returns are generated?

How large is the sukuk market in the sources’ global context?

How does the Maaden sukuk Islamic finance model help global mining investors participate?