Saudi Arabia is building mining capacity at home while also setting up routes to participate in global minerals supply chains. One way to read the strategy is through how capital is being organized and deployed. Discovery Alert reports that the Saudi Mining Development Company (Ma’aden) acts as both an operator and an investment vehicle, with allocated capital exceeding $15 billion for mineral sector expansion through 2030. That kind of balance-sheet backing can support exploration, project development, and downstream buildout, while also creating room for international partnerships that can add expertise, processing links, or new resources.

The Kingdom’s domestic pipeline is expanding quickly, which helps explain why an overseas-facing vehicle can be relevant rather than distracting. S&P Global notes that the number of projects drilled rose to 160 in 2024 from 58 in 2023. Discovery Alert also describes active projects climbing to over 160 in 2024 compared with 15 in 2020. Vision 2030 targets mining’s GDP contribution at 240 billion Saudi Arabian riyals (US$64 billion) by 2030, along with 200,000 direct and indirect jobs and US$27 billion in new investment. Those figures set a clear demand signal for capital, technology, and secure access to minerals.

How Overseas Stakes Fit the Domestic Mining Push

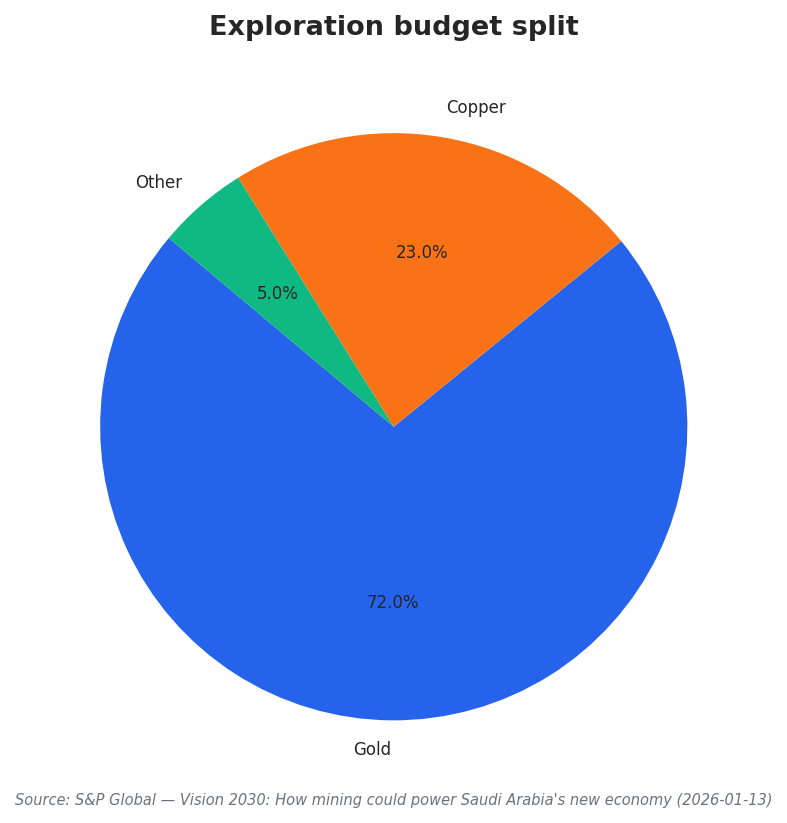

Overseas assets can be used to complement local reserves and accelerate learning curves in specific commodities and operating models. One example already disclosed is from Futurism, which says Manara Minerals Investment Company secured a 10% equity position in Vale Base Metals. In parallel, S&P Global reports that 72% of Saudi Arabia’s total exploration budget in 2025 went to gold and 23% to copper, while copper reserve life is estimated at 15 years and gold at 40 years. That mix suggests why external positions can be used to broaden optionality and support supply chain participation alongside local exploration and mine development.

Policy and incentives are also shaping how capital can be mobilized across the value chain. Futurism reports that the Mining Investment Law reduced tax rates from 45% to 20%. The same source says a USD 182 million exploration incentive program covers up to 25% of exploration costs and 75% of development costs through the Saudi Fund for Development, and that active mining permits reached 2,485 with exploration licenses growing 350% since reforms began. In practice, these tools can make domestic projects more bankable, which can then sit alongside international stakes inside a broader Saudi Arabia mining investment fund approach to overseas assets.

Equipment and exploration services are scaling in step with this investment posture, reinforcing that the shift is operational, not just financial. Mordor Intelligence estimates the Saudi Arabia mining equipment market at USD 7.32 billion in 2025 and expects it to reach USD 9.72 billion by 2030 at a CAGR of 5.83%. It also reports that diesel held a 75.16% share in 2024, while battery-electric is forecast to grow at a 16.31% CAGR between 2025 and 2030. Separately, Futurism cites IMARC data valuing the Saudi Arabia mineral exploration equipment market at USD 2,052.5 million in 2025. Together, these figures show the operational capacity building that can make overseas minority positions more valuable by connecting them to a scaling domestic ecosystem.

What signals that Saudi Arabia is backing mining with large capital plans?

How fast is Saudi Arabia’s drilling and project activity growing?

What is a concrete example of Saudi-linked overseas mining exposure?

How do incentives and reforms support a mining investment fund focused on overseas assets?

What do market estimates say about mining equipment demand inside Saudi Arabia?