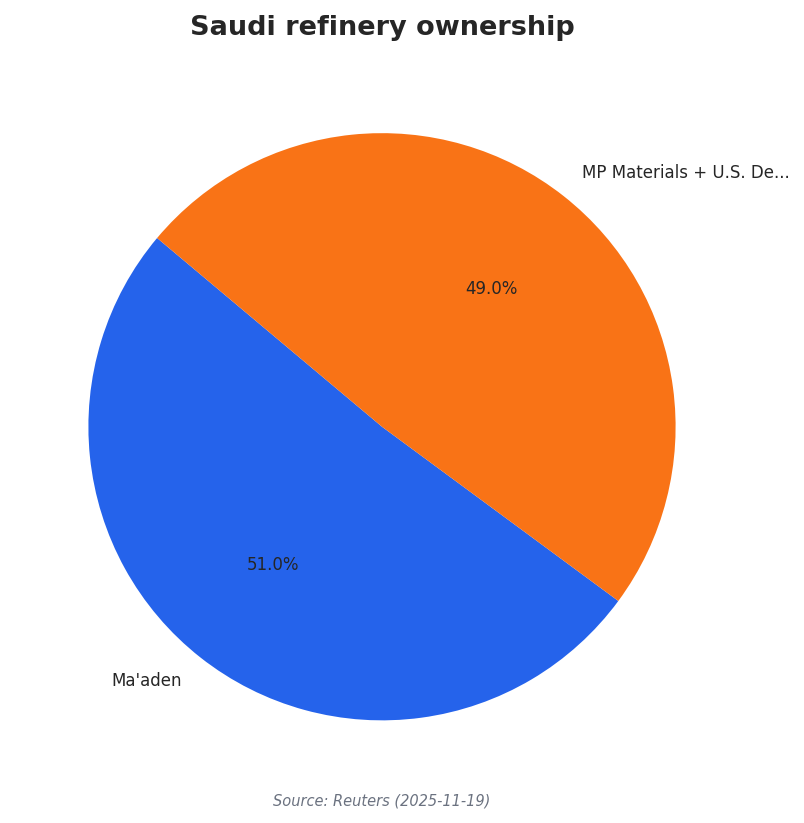

A Saudi-based rare earth refining joint venture has moved from speculation to a defined structure. Reuters reports that Ma’aden will hold 51% of the refinery, while MP Materials and the U.S. Department of Defense (DoD), through a joint venture, will hold a combined 49%. Shanghai Metals Market (SMM) adds that the DoD will provide non-recourse funding and MP Materials will contribute rare earth separation and refining technology. In early trading after the announcement, SMM says MP Materials’ stock rose by over 10%. The stated ambition is practical: create additional processing routes outside China for separated light and heavy rare earth oxides, which are needed downstream for metals, alloys, and magnets.

The refinery’s logic sits in the “middle” of the value chain, where separation and processing can become the true bottleneck. MP Materials’ CFO Ryan Corbett told Investing News that headlines often over-focus on either mining or magnets, while the hardest parts live in between. He described multiple steps from oxide to finished magnets, including converting oxide to metal, then alloy flake, then powder, followed by pressing, sintering, slicing, and grinding. Corbett also warned about ambitious magnet-plant announcements from groups that “have never made metal before,” stressing the need for time, investment, R&D, and experience. That framing helps explain why a new Saudi processing node is more than a headline about a single facility.

How the Stake Split, Funding, and Feedstock Shape the Project

Two points define the joint venture’s governance and execution incentives. First is control: under both Reuters and SMM, Ma’aden holds at least 51%, preserving Saudi leadership over the project. Second is the financial and technical pairing: SMM describes a “resource-for-technology model,” with Saudi Arabia providing resources and capital while MP Materials brings separation and refining know-how, supported by U.S. government involvement. SMM also notes that as early as July 2025, the Pentagon acquired a $400 million stake in MP Materials, becoming its largest shareholder, and frames the Saudi project as an extension of the DoD’s approach to building alternatives to China through allied systems.

Supply-chain implications are most acute for heavy rare earths, where China’s dominance is most concentrated. CSIS states that as of 2023, China accounted for 99% of global heavy rare earth element (HREE) processing, and it highlights risks created by export restrictions and a 2023 global ban on exporting rare earth processing and separation technologies. Reuters adds a company-level constraint: MP Materials has struggled in the United States to find supplies of dysprosium and terbium, two heavy rare earths used in magnets for electric vehicles, fighter jets, and other products. In this context, the rare earth refinery Saudi Arabia MP Materials partnership signals an attempt to diversify processing routes and improve resilience where dependence is most extreme.

Saudi Arabia’s resource narrative is part of the pitch, but it comes with execution risk. SMM cites an assessment by the Saudi Geological Survey estimating approximately 3.2 million mt of rare earth reserves in Saudi Arabia, accounting for 1.5% of the global total. It also cites the Jabal Sayid deposit with about 552,000 mt of heavy rare earth and 355,000 mt of light rare earth resources, and says it is estimated to potentially be the world’s fourth most valuable rare earth reserve. Yet Rare Earth Exchanges cautions that “scaling is brutal” and that heavy rare-earth feed remains “the hard part.” For Western supply chains, the refinery is less a finish line than a new midstream foothold that still must prove throughput, reliability, and repeatable output quality.

Who owns the Saudi rare earth refinery joint venture?

What will the refinery produce?

Why does heavy rare earth processing matter for Western supply chains?

How does the MP Materials–Ma’aden refinery in Saudi Arabia relate to U.S. defense involvement?

What resource figures are cited for Saudi Arabia’s rare earth potential?