Saudi Arabia is working to strengthen a more complete mining-to-metals chain, and steel is central to that story. Hadeed is one of the key players named in Saudi Arabia’s structural steel market landscape, and it is also described as a prominent integrated steel facility in Al Jubail that was established in 1979 and began operations in 1983. Expansion is now framed as both an industrial capability move and an import-substitution move. In 2023, Saudi Arabia imported approximately 2 million tonnes of steel, accounting for 20% of total consumption, according to a KSA iron and steel market outlook. That import exposure is one reason new capacity and modernization programs are being watched closely.

Several sources point to Hadeed-specific steps that build toward a larger domestic supply base. One outlook states that an upgraded Hadeed plant, including energy-efficient furnaces and advanced automation systems, will increase production capacity by 25% upon completion in 2025. Separately, another market update says national producers such as Hadeed are moving large-scale hot-strip-mill expansions scheduled to start in 2026, adding roughly 2.5 million tonnes per year of capacity, with the aim of replacing the bulk of imported flat steel with local production. These moves connect steelmaking upgrades to a broader “from input to product” backbone, where reliable local output supports downstream users across construction and industry.

Why Demand Signals Support More Local Steel Capacity

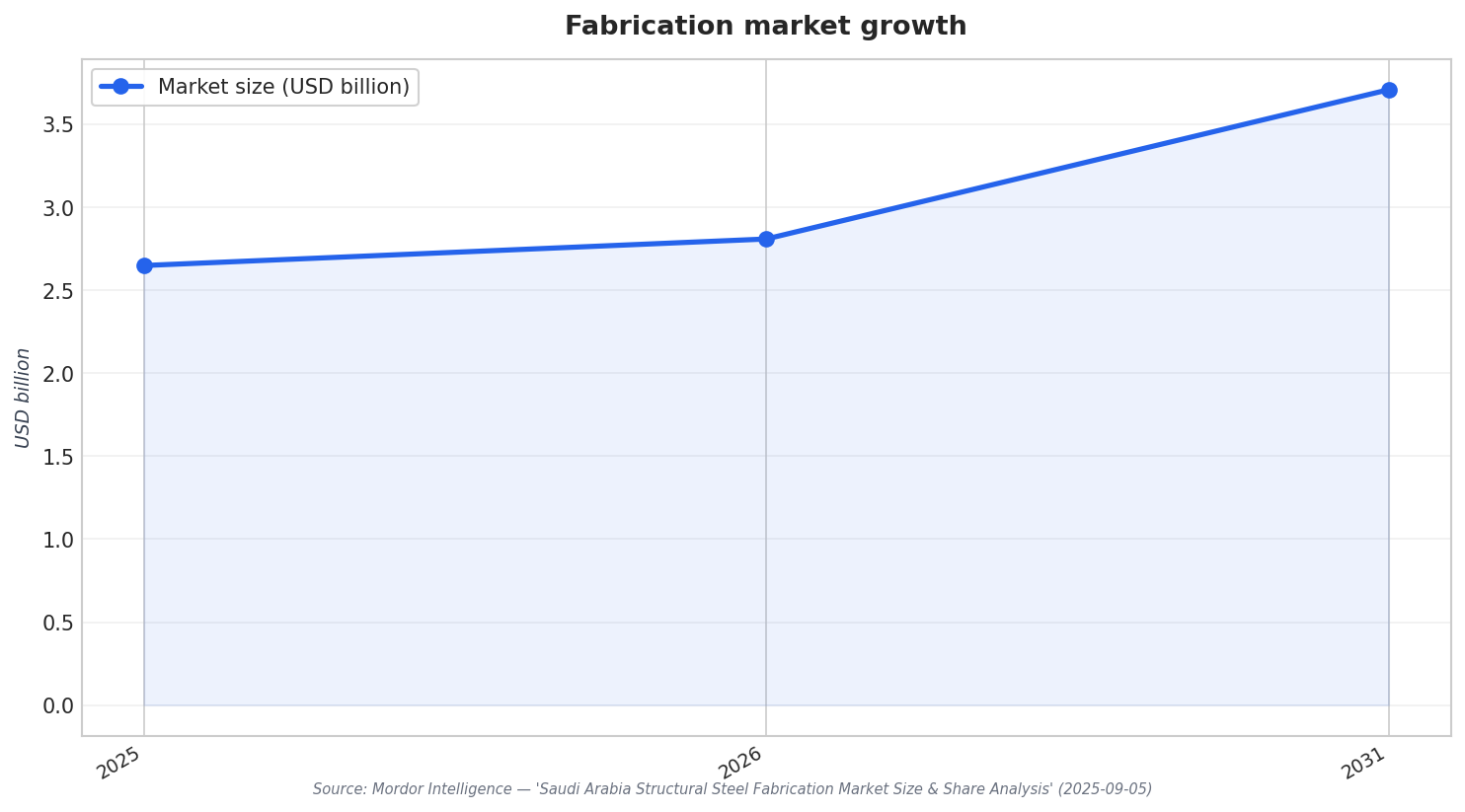

Demand pull from fabrication and construction is also quantified in recent market research. Mordor Intelligence values the Saudi Arabia structural steel fabrication market at USD 2.65 billion in 2025, estimating growth from USD 2.81 billion in 2026 to USD 3.71 billion by 2031 at a CAGR of 5.77% for 2026–2031. The same report adds detail on where steel is being consumed: oil and gas held 32.1% share in 2025, while power and energy is projected to grow at an 8.4% CAGR through 2031. It also notes the Eastern Province captured 36.88% of market size in 2025, while Riyadh Province is projected to expand at a 7.01% CAGR through 2031, reflecting where workshops and project sites are concentrated.

Capacity additions are not limited to one company, which matters for how a national mining-to-metals backbone takes shape. An April 2026 update says Saudi Arabia launched its first integrated steel plate complex in Ras Al-Khair, using gas-based DRI and electric-arc furnaces, adding about 1.5 million tonnes of annual plate capacity. Beyond that, Essar is cited as having launched a USD 4 billion Saudi steel plant aimed at a low-carbon steel facility with 4 million tons of annual production capacity in Ras Al-Khair. Another industrial equipment-focused source also references new integrated steel projects, including Essar’s USD 4 billion flat steel complex at Ras Al-Khair Industrial City and Tosyali Holding investing USD 3.6 billion in a new steel plant, underscoring that the broader ecosystem is scaling alongside Hadeed.

Policy, industrial investment, and licensing momentum provide additional context for sustained build-out. One market commentary states that regulatory reforms have triggered a 95% surge in new investments and a 267% rise in manufacturing licenses, while Saudi crude steel production capacity now stands at around 12 million tons annually. Separately, an equipment market article reports that Saudi Arabia’s factory count grew from 7,206 in 2016 to 11,549 by 2023, with SAR 81 billion in new industrial investment recorded in 2023 alone, and over SAR 3.1 billion going into industrial zone infrastructure. Within this backdrop, the Hadeed steel expansion in Saudi Arabia is best understood as a practical lever: more upgraded capacity, more local flat steel availability, and a tighter link between upstream industrial priorities and downstream fabrication demand.

What does the Hadeed steel expansion in Saudi Arabia add in flat steel capacity?

How much could Hadeed’s upgraded plant lift production capacity?

How big is Saudi Arabia’s structural steel fabrication market, and what growth is expected?

What new plate capacity was reported for Ras Al-Khair in 2026?

How significant are steel imports in Saudi Arabia, based on the cited sources?