Mineral processing in Saudi Arabia is moving to the center of Vision 2030. The goal is clear: do more than extract and export. Saudi Arabia wants to turn mineral resources into industrial strength through processing, refining, manufacturing, and trade partnerships. This shift supports economic diversification and helps build local value chains that can serve fast-growing energy transition industries.

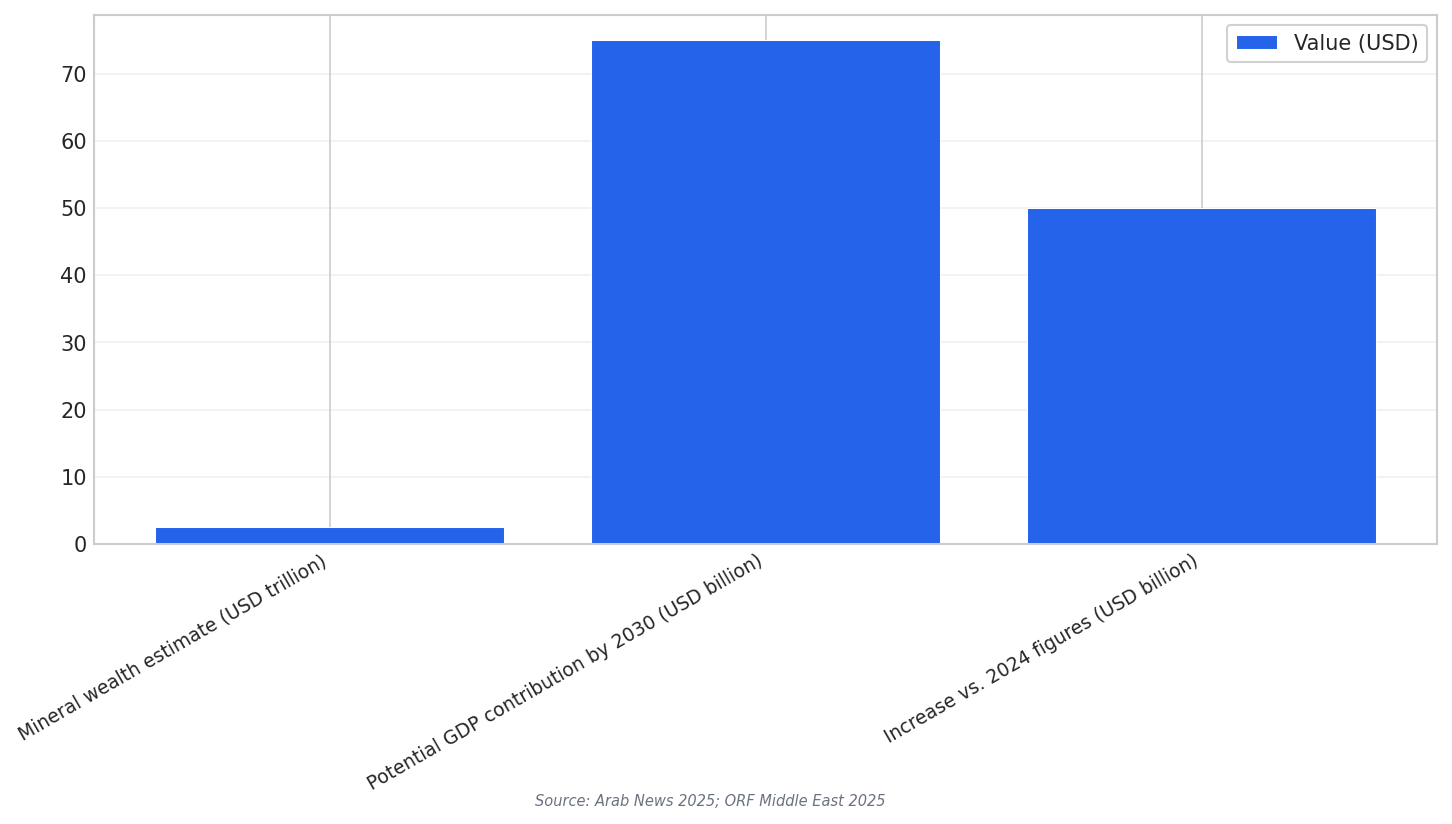

Several targets and figures show why this push matters. One Arab News report values Saudi Arabia’s mineral wealth at SR9.4 trillion ($2.5 trillion). Another analysis says a systemic expansion of the mining sector, plus critical minerals processing capacity, could contribute close to US$75 billion to GDP by 2030. It also describes this as an increase of more than US$50 billion from 2024 figures.

The strategy is not only about digging more. It is about building capacity in processing, which ORF Middle East calls a crucial bottleneck in global supply chains, even in countries that have the minerals. Processing know-how can also support downstream sectors such as magnet production and advanced electronics manufacturing. This creates a vertical of value that can strengthen the broader diversification plan.

Why Downstream Clusters Matter More Than Raw Output

Saudi Arabia is also developing integrated industrial clusters where extraction, refining, and manufacturing can sit closer together. Arab News highlights site development including Oxagon and Ras Al-Khair, plus legislative reforms such as the Mining Investment Law. In the same coverage, one expert said co-locating extraction, refining, and manufacturing has led to double-digit percentage reductions in logistics costs. The message is simple: integration can cut friction and make midstream activity more competitive.

This is also about picking minerals and projects that match real market demand. Arab News reports that Saudi Arabia’s “most realistic advantage” in the energy transition is combining selective mining with strong processing and refining capabilities, supported by its emerging role as a logistics and supply-chain hub. The Kingdom’s position between Africa, Europe, and Asia is presented as an advantage for downstream processing and value-added industries.

Vision 2030’s mining strategy also names specific downstream directions. It targets fertiliser production from phosphate, aluminium rolling and fabrication, copper smelting, and mineral-based industrial products. Arab News also stresses integrating mining with downstream industries such as aluminum smelting, phosphate processing, and electric vehicle battery production. Another Arab News report adds that Saudi Arabia has secured lithium processing capabilities, becoming the first Middle Eastern country to establish a battery materials supply pipeline.

What does “mineral processing in Saudi Arabia” mean in Vision 2030 terms?

How big is Saudi Arabia’s mineral opportunity, based on the sources?

Why does Saudi Arabia want integrated mining and industrial clusters?

Which downstream industries are highlighted as priorities?