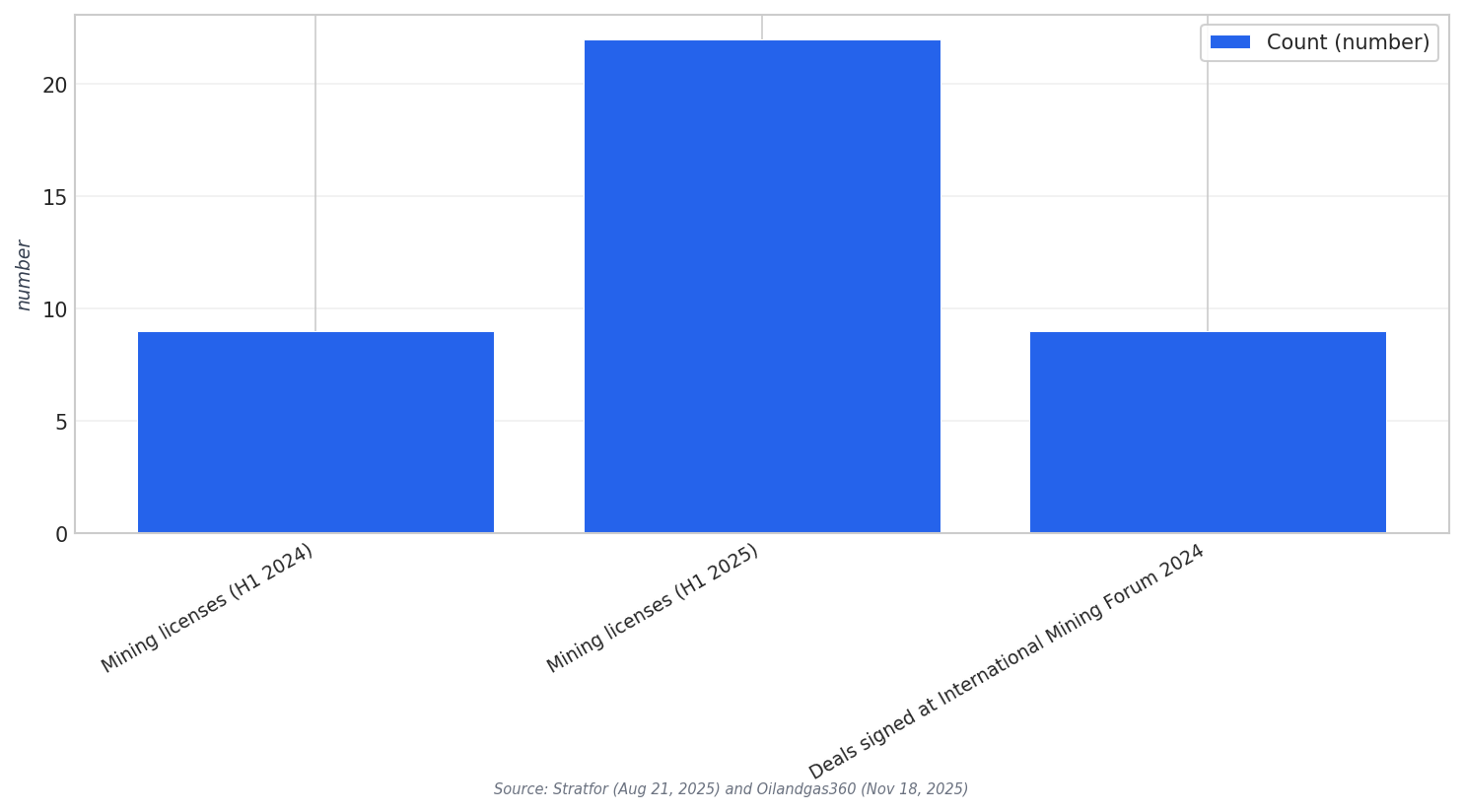

Saudi Arabia is pushing mining from a supporting sector into a strategic one. New exploration licenses have been awarded to Ajlan & Bros with China’s Zijin Mining and to India’s Vedanta. Those licenses cover nearly 4,800 square kilometers of copper, zinc, gold, and silver prospects. The speed of permitting is also rising. In the first six months of 2025, Saudi Arabia issued 22 mining licenses, up from nine during the same period in 2024. This licensing momentum sits behind the wider story of Saudi China mining cooperation and how Riyadh is using partnerships to build capabilities.

Saudi deal-making has also become more visible at major events. At the International Mining Forum 2024 in Riyadh, nine metals and mining deals worth more than $9bn were signed. Examples included a copper project by Vedanta at Ras al-Khair and a phased zinc–lithium–copper complex by Zijin. At the same time, outside observers have warned that Chinese involvement and possible high interest in other projects could shape the Kingdom’s direction. In this framing, metals and minerals are described as geopolitical-geo-economic power-play instruments, with Washington and Beijing competing.

From Licenses to Leverage: Processing and Battery Metals

Riyadh’s next step is not only to issue permits, but to climb the value chain. Saudi mining giant Ma’aden is central to this domestic build-out. It is majority-owned by PIF at around 65%, and another report cites 63.9% ownership by the Public Investment Fund. Ma’aden has ramped up production in gold, phosphates, and aluminum, and is now targeting copper and increasingly lithium. A non-binding term sheet with Aramco and KAUST explores a minerals venture focused on energy-transition metals, including lithium extraction from unconventional sources. Saudi Arabia wants to produce, not just import, battery metals by the late 2020s.

Saudi strategy is also shaped by China’s position in global refining and upstream assets. One constraint is described as China’s processing dominance and its grip on many upstream projects. CNN, citing the International Energy Agency, says China controls over 90% of the world’s output of refined rare earths and over 60% of rare earth mining production. Saudi officials and analysts increasingly discuss processing more minerals in the Kingdom, and Saudi Arabia’s exploratory mining budget increased 595% between 2021 and 2025, according to S&P Global. The direction is clear: licensing and exploration are paired with ambitions for processing hubs.

China’s wider battery metals strategy in Africa adds context to why Saudi China mining cooperation matters. Business Insider Africa reports that Chinese firms have expanded dominance in Africa’s mining sector through acquisitions and equity stakes, securing critical minerals such as lithium, cobalt, and copper. It also reports Huayou Cobalt’s planned acquisition of Atlantic Lithium for $210 million, with all issued shares acquired at $0.25 each, valuing Atlantic Lithium at about $210 million. For Saudi Arabia, this global competition runs in parallel to domestic reform and licensing. Brunswick Exploration’s CEO described a transparent and modern process to obtain exploration licenses in Saudi Arabia, while noting a few hiccups along the way.

What is Saudi China mining cooperation in this context?

How large are the new exploration license areas tied to Zijin and partners?

What deals highlighted Zijin’s role at the International Mining Forum 2024?

How fast is Saudi Arabia increasing mining licenses?

Why does processing matter in the Saudi minerals strategy?